What is Japan Earthquake Insurance for Earthquake Preparedness? – About its Necessity and Basic System

Japan is an earthquake-prone country, and there is a history of discussions and studies over a long period of time before the earthquake insurance system was introduced. In the wake of the 1964 Niigata Earthquake, the government and property & casualty insurance companies researched and drafted a law concerning earthquake insurance, and the system that continues to this day was launched. Since it is difficult to predict the occurrence of fires and damages to buildings due to earthquakes and volcanic eruptions, but such damages are often enormous, earthquake insurance became highly public insurance jointly operated by the government and property & casualty insurance companies. In addition, earthquake insurance cannot be taken out by itself, and it must be taken out together with fire insurance.

*The guidelines for earthquake insurance in Japan are constantly being revised. We recommend that you contact and consult your insurance company for coverage, premiums, and deductibles.

What is Earthquake Insurance?

Earthquake insurance in Japan pays insurance money when a building or household properties covered by earthquake insurance is damaged by a fire, destruction, burial, or flood loss caused by an earthquake, volcanic eruption, or tsunami due to any of these.

What is covered by earthquake insurance?

Earthquake insurance covers "buildings" and "household goods" in the same way as fire insurance. You can select the options among the "Buildings Only", "Household Goods Only", and "Buildings and Household Goods".

What is the coverage period of earthquake insurance?

You can choose from short-term (1 year) and long-term (2-5 years). As with fire insurance, the longer the insurance period, the less the insurance premium per year.

How much insurance money can you receive?

Earthquake insurance contract shall be made for each of a building and household goods. The coverage amount of earthquake insurance is usually within the range of 30-50% of the coverage amount of fire insurance. The maximum coverage amount is 50 million yen for a building and 10 million yen for household goods.

[Example]

-In case of Fire insurance for Building at the coverage amount of 20 million yen, and for Household goods at the coverage amount of 10 million yen,

-Earthquake insurance for Building, which can be set at the coverage amount of 6 - 10 million yen, and for Household goods, which can be set at the coverage amount of 3 million - 5 million yen.

How is the indemnification amount determined?

A property & casualty insurance company confirms the status of damage to buildings and household goods and determines which of the following four categories according to the degree of damage: " Total loss ", " Large half loss ", " Small half loss ", and " Partial loss ". If it is less than "partial loss", it will not be eligible for compensation.

Total loss: 100% of the insured amount (limited to the market value)

Large half loss: 60% of the insured amount (limited to 60% of the market value)

Small half loss: 30% of the insured amount (limited to 30% of the market value)

Partial loss: 5% of the insured amount (limited to 5% of the market value)

[Example]

- In case of Fire insurance for Building at the coverage amount of 20 million yen, and for Household goods at the coverage amount of 10 million yen, and Earthquake insurance for Building at the coverage Redof the building (foundations, pillars, walls, roofs, etc.) is 50% or over of the market value of the building, the extent of the damage shall be “Total loss”.

Insurance money to be paid: 10million yen x 100% = 10 million yen

- With damage caused by an earthquake, cases where the amount of damage to household goods is 60% or over, the extent of the damage shall be “Large half loss”.

Insurance money to be paid: 5million yen x 60% = 3million yen

How are Premiums for the Earthquake Insurance determined?

Answer: Earthquake insurance premiums vary depending on “the structure of the building" and "the location of the building", and the insurance premiums are calculated and determined according to the risk of the building.

About the structure of the building

Considering the risk of damage caused by earthquake shaking and destruction by fire, the structure of buildings is divided into two ranks: wooden and non-wooden structures (steel frames, reinforced concrete structures, etc.). Wooden structures have high risk of damage and destruction, and insurance premiums may be high while non-wooden structures have low risk and insurance premiums may be low.

In addition, the following discounts are applicable depending on the building's year of construction, seismic rating, and structure. (Only one discount can be applied and cannot be duplicated.)

Discount System of Earthquake Insurance

| Name of discount | Rate of discount | Description of discount |

| 1.Seismic isolated building discount | 50% |

Cases where the insured building is a seismic-isolated building pursuant to the Housing Quality Assurance Act |

| 2.Seismic grade discount | Seismic Grade 1 10% Seismic Grade 2 30% Seismic Grade 3 50% |

Cases where the insured building has a Seismic Grade (preventing the collapse of the structural framework) as stipulated in the "Housing Performance Labeling System" based on the " Housing Quality Assurance Promotion Act" |

| 3.Earthquake-resistance diagnosis discount | 10% |

Cases where the insured building satisfies the earthquake-resistance standards set forth in the Building Standards Act (effective on June 1, 1981) as a result of an earthquake- resistance diagnosis conducted by local governments, etc. or seismic retrofitting. |

| 4. Age of building discount | 10% |

Cases where the insured building is one that was constructed after June 1, 1981 |

About the location of the building

The basic rate of Insurance Premiums for each prefecture is determined according to the risk of an earthquake.

You can check it on the website of the Ministry of Finance.

Basic Rate of Premiums for the Earthquake Insurance

[Example]

Location: Tokyo

Premium for one year for the insurance amount of 10million yen: 27,500 yen

Structure: Reinforced concrete structure, built in 2000

Earthquake Insurance coverage for: Building only

Insurance amount: 10 million yen

Contract period: 2 years (long-term coefficient 1.90)

Age of building discount: 10%

Insurance premium 27,500 yen × 0.9 (10% discount) × 1.90 = 47,025 yen (23,512.5 yen/year)

How does earthquake insurance work for condominiums?

The scope of earthquake insurance coverage for condominiums is divided into "common use space” that is used communally by residents and "exclusive use space” that is used for the owner's residential space. The scope of the same insurance coverage that the condo apartment owner takes out is for “exclusive use space” and “household goods”. For the “common use space” of the condos, the management association takes out the insurance. The common use spaces include shared facilities, hallways, exterior walls, entrances, etc. as well as balconies and entrance doors attached to the residential units.

How is the damage of condominiums determined?

In case of condominiums, the damage of the exclusive use space (which is insured by the owner) is generally determined as the same as the damage situation which is determined for the common use space. If the common use space is determined as partial loss, the exclusive use space will also be determined as partial loss even though there is no damage to the space. If the determination differs from the actual damage situation, you can also request a re-examination individually.

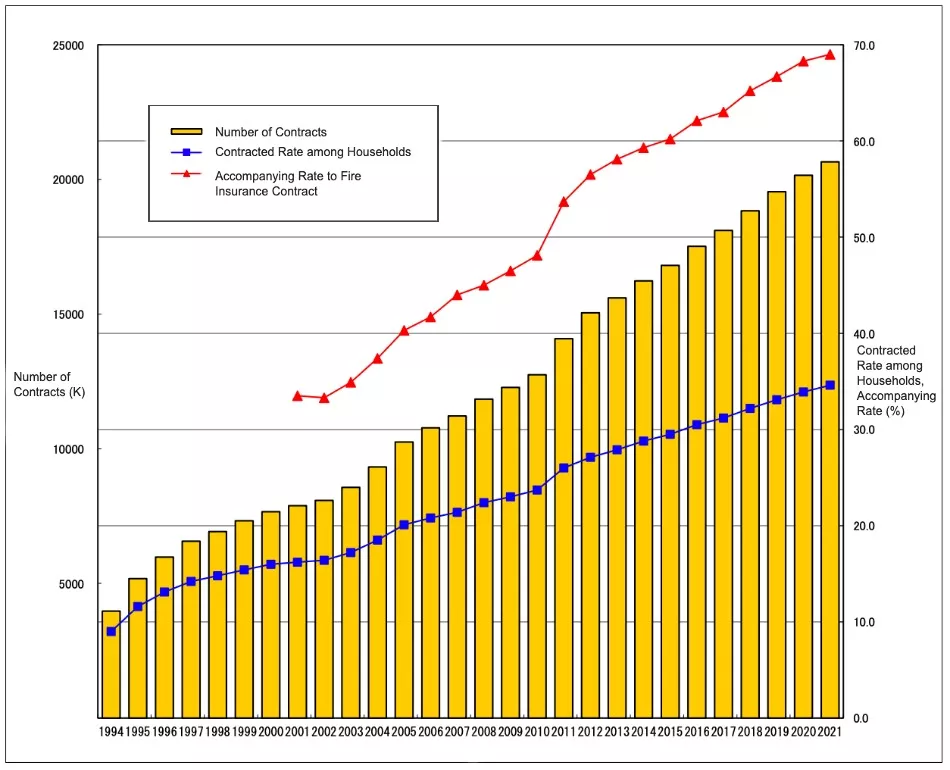

What is the Contracted Rate of Earthquake Insurance?

According to data from the Cabinet Office in fiscal 2015, the contracted rate of fire insurance is 82%, which is a high level for a voluntary insurance contract. The contracted rate of earthquake insurance is 33.9% according to Statistics Compiled by General Insurance Rating Organization of Japan" (Fiscal 2020). “Accompanying rate of earthquake insurance”, which is the percentage of people who attached earthquake insurance to fire insurance contracts, was 68.3% in fiscal 2020. In the areas where major earthquakes are predicted in the future or where a major earthquake have occurred recently, the contracted rate or accompanying rate of earthquake insurance among households is higher than the other areas.

Changes in the Number of Contracts, Contracted Rate among Households, and Accompanying Rate of Earthquake Insurance

Data Source: General Insurance Rating Organization of Japan

Data Source: General Insurance Rating Organization of Japan

The Accompanying rate is higher among households of condominiums than those of detached houses.

As of 2013, the percentage of earthquake insurance coverage for the exclusive use space among condominium residents was 70.9%. The accompanying rate of earthquake insurance for all residences (condominiums and detached houses) in the same fiscal year was 58.1%, so it can be said that the accompanying rate of earthquake insurance is higher among households of condominiums than those of detached houses. The reason is that the premium for earthquake insurance for condominiums is only applicable to the exclusive use spaces and is less expensive than that for detached houses. Why is the insurance premium for condominiums is inexpensive? Because condominiums are non-wooden buildings with lower risk of damages against earthquakes than detached houses with many wooden structures.

Insurance for the Common Use Space of Condominiums

According to data from the Ministry of Finance, the earthquake insurance accompanying rate for the common use space of condominiums, which the management associations take out, was 37.4% as of 2013. While 93.2% of the management associations take out fire insurance, this accompanying rate is quite low. Among many newly built condominiums in particular, their management associations have not yet taken out earthquake insurance. The reasons are that insurance premiums are high, and many people see that condominiums are robust and will not collapse.

Are there Tax deductions for the Earthquake Insurance premiums?

Tax deduction system for earthquake insurance allows the maximum of 50,000 yen for income tax (national tax) and the maximum of 25,000 yen for inhabitants tax (local tax) to be deducted from gross income.

Are There Bilingual Insurance Agents?

There are bilingual insurance agents who handle fire insurance, and they can provide assistance in English in the event of an incident or accident in addition to an estimate.

For more information on insurance and bilingual agents, please see A Simple Guide to Home Insurance in Japan.

Is earthquake insurance necessary?

Earthquake insurance does not cover all the damages to buildings and household goods but is an insurance to support life after a disaster. In the event of an earthquake, you can receive compensation under a public support system called the " Act on Support for Reconstructing the Livelihoods of Disaster Victims," but the maximum amount paid is about 3 million yen, which is not enough. Expenses assumed in the event of a major earthquake may become quite large, such as the cost of large-scale repairs and reconstruction, housing loan repayments, the rent of a new house, and the expenses for rebuilding your life. We recommend that you simulate the risk of damage caused by an earthquake and the expenses necessary to rebuild your livelihood and consider the necessity of earthquake insurance.

- Apartments and Houses for Rent in Tokyo

- Listings of popular and luxurious rental apartments, condominiums, and houses designed with expats in mind.

- Apartments and Houses for Sale in Tokyo

- Listings of apartments, condominiums, and houses available for purchase in Tokyo.